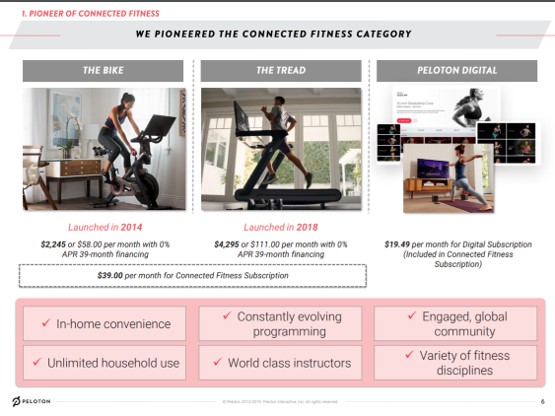

Peloton Interactive, which became public last September, published its Q2, 2020 earnings report yesterday (Feb 5). The company, which sells connected fitness devices and digital content, experienced a YoY growth of +77% in revenue, with sales for Q2 standing at $466 million. According to the company’s Q1, 2020 presentation, Connected Fitness Products (bikes and treads) account for almost 80% of revenues. The company expects the revenue for full year 2020 (ending June, 2020) to reach $1.53 – $1.55 billion, higher than projected in the Q1 report.

Peloton now has 712,000 connected fitness subscribers (i.e., people with either a Peloton Bike or a Peloton Treadmill, as well as the digital subscription) and over 2 million members when considering overall digital users. I am one of those connected fitness subscribers and a walking, running, riding and stretching example of the addictive effect of Peloton; and as a year-long user, and 20-year long market researcher and consultant, I was curious to dissect the company’s hits and misses. Here are my insights.

“Engaging-to-the-point-of-addictive”

Peloton is sometimes speculated as a fitness “fad”. But an extremely low churn rate by any subscription model standards suggests otherwise. It is better described as a phenomenon, a disruptor, a long-term trend leader with a cult following, at the crossway between physical wellness and mental wellness (see our Stress-Free as a growth engine report from Feb 2017 to learn why this is so important).

Retention is explained, in the Q1 report, as stemming from “engaging-to-the-point-of-addictive fitness”. Indeed, Peloton’s usage statistics are the best proof for the content’s stickiness. The connected fitness subscribers worked out with Peloton over 24.3 million times in Q2, averaging 12.6 monthly workouts per connected fitness subscriber, up from 9.7 monthly workouts in the same period a year ago, according to the company. This means that consumers, who have gotten used to paying for fitness services they will not use – such as gym memberships – are not only trying out the classes, but are increasing their exercise frequency.

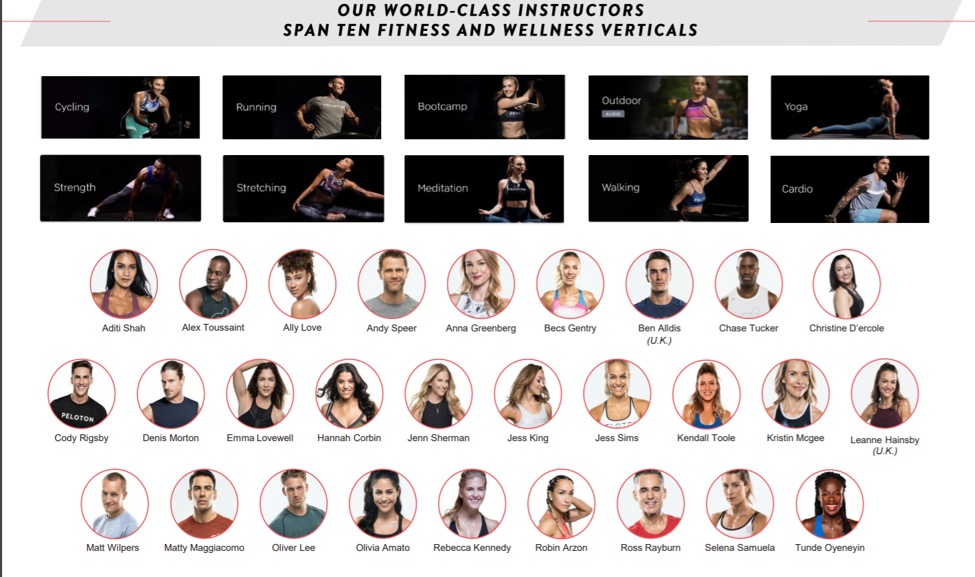

Variety, which increases consumers’ perception of value and is directly linked to loyalty and retention, is achieved by offering many classes in 10 different verticals, as well as by making the classes varied in content, music, structure, duration, goals, difficulty level and character. This resulted in a low average net monthly connected fitness subscriber churn of 0.74% in Q2. Moreover, the company’s world-class hand-picked instructors are known for their differences, creating more variety (and spurring long discussions on favorite instructors – more on that later).

Getting there first

The company recognized, in its Q1 2020 report, that consumers are increasingly searching for better value for money, getting more in less time, enjoying a wider content selection and determining when, how and where to consume content, be it music, television, gaming, books, and news. The benchmark is, therefore, content companies such as Netflix and Amazon. But Peloton can also be compared to the likes of Airbnb and Uber: Peloton taps into a huge traditional industry (fitness products and services) and, using technology, not only sways current users into the digital alternative, but also attracts new consumers that are incremental to the industry. And, like Uber and Airbnb, it enjoys the fact it is the pioneer, the main beneficiary of the Network Effect – key to its future growth.

(Q1 2020 slide. In Q2 2020 the price for Digital Subscription decreased to $12.99)

Peloton is not the only competitor in the connected fitness category. In the last few years, CES and similar shows exhibited connected fitness at-home solutions, from gaming to smart mirrors, and Peloton’s success was by itself a huge booster for the category, attracting both existing hardware manufacturers who are entering software and content, and newcomers who are trying to disrupt the disruptor by offering lower-priced alternatives. The prominent examples are probably Echelon and Flywheel, the legal battle with whom is discussed on this WSJ article. Flywheel just settled with Peloton, admitting to copy its Leader Board technology, this February.

The rising competition does not stop there. There’s an influx in digital workout apps, all competing for the Gen Y/ Gen Z time-deprived wellness-seeking consumer. And while Peloton’s connected equipment users are less likely to leave, the company must differentiate itself from its growing competition to avoid the murky waters of the variety-seeking consumer (a big culprit in many meal-kit services shut-downs).

Consumer Loyalty is Key

Peloton’s decision to lower its digital-only monthly subscription fees, from $19.49 to $12.99, looks at first glance like a race to the bottom, mainly as profitability will not be attained until 2023. But underlying is the company’s assumption that people who use the app, are more likely to eventually get the bike – weather because they wish to participate in the community and “Leader Board” or because they wish to embrace the lifestyle. If consumers do purchase the connected equipment, they are presumably locked-in for the long run, as well as generate higher revenue.

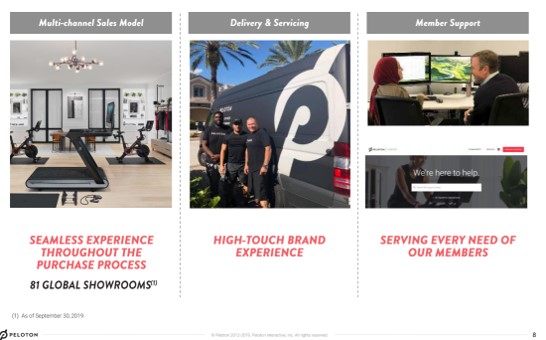

The company briefly discussed some of its advantage amidst the competition. One of the claims is the omni-channel strategy, covering trial, sales, content and service. It’s studios and showrooms in more than 80 locations globally are supposedly serving as a differentiator, and the company therefore invests in new locations (including a “super studio” in NYC).

Peloton is also partnering with physical locations such as hotel chains and workplaces, to increase exposure to the content and equipment. But competitors can beat Peloton to the goal by partnering with a variety of fitness-oriented outlets. This is why, in my opinion, the company should be leveraging the physical points of sale (and studios) more.

As I’ve mentioned, the company’s biggest competitive advantage at the moment, is the fact it pioneered the category. This, in turn, creates a network-effect: Peloton is extremely viral – if your friends have it, you are more likely to consider it. In fact, word of mouth plays a crucial part in the path to purchase. 43% of peloton buyers in FY 2019 first heard about it from a family member or a friend – up from 23% in 2017. And, once your friends are there – you are more likely to stay with the company, where you can connect with your friends through the Leader Board. This is another potentially huge deal for the company, which currently feels overlooked. First of all, referrals are rewarded, but are not actively encouraged. Here, the fact that the company has physical locations and studio classes could have been leveraged to friend invitations / shared experiences (take a page out of the ClassPass book). Events and parties, to grow the user’s community beyond the friends they are already connected to on another social network, can create more stickiness and increase the network effect.

In my opinion, the company’s biggest overlooked asset (beyond data, which I will not discuss in this article) – is just that: the communities that form on other platforms. These include endless “tribes” (around physical attributes, mutual interests/goals, and of course – trainers), posts, stories and discussions, that are taking place on Redditt, Instagram, Facebook, and countless other virtual groups – none of which is controlled by, or enhanced by, Peloton. Peloton can increase partner sales, user-generated new revenue, and loyalty, by forming (or “hosting”) a community; rewarding it, engaging it in events and helping people find like-minded friends. The strength of a community is probably the reason why the “Leader Board” is at the heart of the Peloton technology, and why other competitors are trying to copy it. Peloton is well-positioned to tap into this community on all fronts.

Lastly, a differentiating asset that is acknowledged by the company is its talented, super-charismatic, and characteristically diverse instructors. Peloton users are passionately debating the pros, cons and everything in-between, of each instructor, on said social platforms. But just as HBO’s subscription base grew and fell with Game of Thrones, so should Peloton focus on retaining its talents, alas consumers might follow them elsewhere. If the reflection on social media is any indication, the company seems to be doing just that – engaging and rewarding its trainers and letting them shine, so that they, in turn, can create their own engaging and motivating content (as with all influencers, the key is to support the Peloton Talents’ content creation). The company should consider making more room to key opinion leaders (such as “tribe” and social group leaders) beyond the sporadical social media communication of “personal stories”.

Looking Forward

The company’s addressable market is massive. In the USA, 67% of ~71 million Millennials, and 64% of ~50 million Gen X consumers engaged in fitness (2019 PHYSICAL ACTIVITY COUNCIL’S OVERVIEW REPORT ON U.S. PARTICIPATION), which makes the addressable market nearly 80 million fitness-oriented consumers. The company breaks down its target demographic to households aged 18-70 with $50+ income, which is 65 million consumers in the US alone. With 2 million users, the beginning of an international journey, a myriad of potential partners from content, hardware, food, accessories, personal care and appliances, to e-commerce, healthcare and financial institutions – Peloton can truly become the biggest lifestyle choice of a stressed-out generation.

Trackbacks/Pingbacks