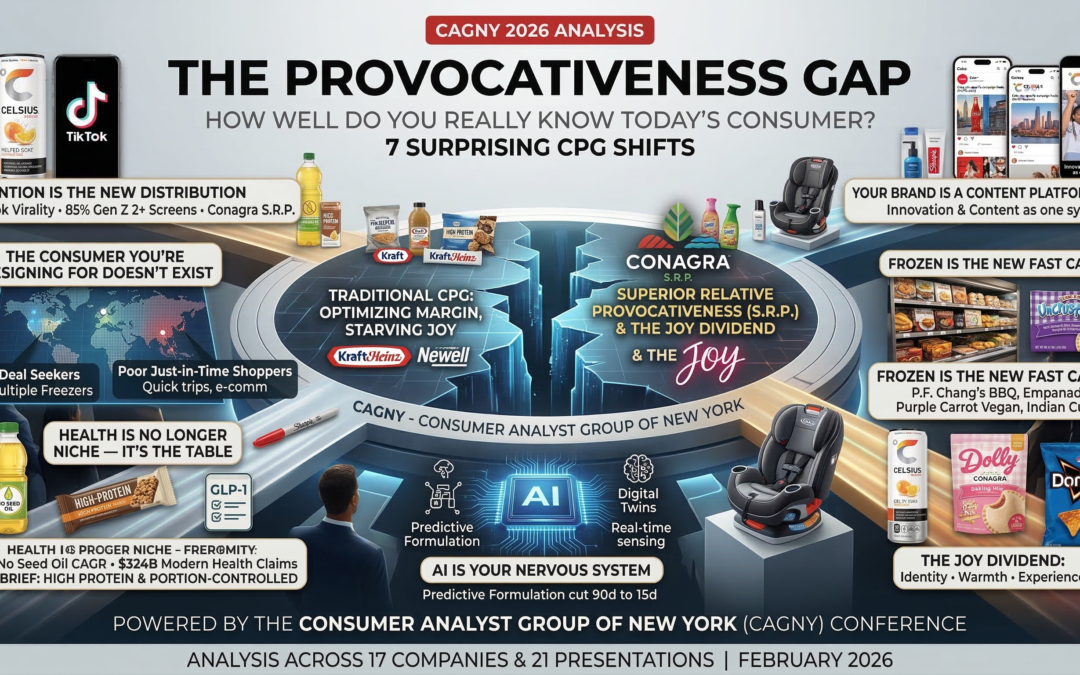

The Provocativeness Gap

How well do you really know today's consumer? 7 surprising insights from CAGNY 2026 that should change how you build brands.

I read 21 CAGNY 2026 presentations and transcripts — from Conagra to Coca-Cola, PepsiCo to Celsius, Mondelez to Newell. What emerged wasn't the usual story of companies weathering a storm or optimizing their way to modest growth. It was something more fundamental: 17 companies simultaneously rewriting the rules of CPG growth, and converging on a set of conclusions that challenge most of what brand teams assume about their consumers.

Here are the seven shifts that stood out — and why they should change how you build brands.

1. Attention Is the New Distribution

Conagra introduced a framework they call "Superior Relative Provocativeness" (S.R.P.) — the argument that winning isn't about being present on shelf. It's about being more provocative than everything else the consumer encounters in a world where attention is fractured across screens, platforms, and 11-second viral cycles.

Sources: Conagra / PWC 2026, TriVision, Datassential, Circana

The result? Conagra claims 60% of its portfolio is holding or gaining volume share — peer-leading — and attributes it specifically to provocativeness, not pricing or distribution. Meanwhile, Hostess (now under Smucker) is cutting 25% of SKUs and closing plants. Same industry, opposite trajectories. The difference is the provocativeness gap.

2. The Consumer You're Designing For Doesn't Exist

Here's a question: who hunts for deals more aggressively — rich consumers or poor consumers?

If you said poor consumers, you're wrong. And you're not alone.

The data from CAGNY tells a story that inverts decades of CPG assumptions. Upper-income consumers are the aggressive deal seekers — 66% more likely to buy on promotion, 2x more likely to own multiple freezers, indexing at 207 for club channel shopping. Their strategy is stock-up-to-save: bigger baskets, fewer trips, maximum deal leverage.

Lower-income consumers? They're just-in-time shoppers. Quick trips, fewer items, navigating the day meal by meal. 68% are either younger habit-builders or retired on fixed income. About 60% don't use SNAP benefits. And they over-index to e-commerce (124 index to total households) — a channel most CPG companies still treat as an afterthought for value-seeking consumers.

The implication is uncomfortable: if your brand strategy targets "mainstream America," you're targeting a demographic that is shrinking in both size and buying power. Every brand needs a bifurcated strategy — or at minimum, a clear answer to the question: which consumer are we actually designing for?

3. Health Is No Longer a Niche — It's the Table

What's the fastest-growing clean-label claim in food and beverage? It's not organic. Not non-GMO. Not gluten-free.

It's no seed oil — growing at a +120% volume CAGR over three years.

Sources: Conagra / Circana, Numerator, NielsenIQ

What started as fringe internet wellness discourse — the kind of thing you'd see in a health influencer's Instagram story — is now reshaping product formulation at scale. Conagra is launching Rebel Roots tallow snack fries and avocado oil popcorn. PepsiCo is restaging Lay's with alternative oil offerings and eliminating artificial colors and flavors across its portfolio. Ingredion says the fiber fortification market is entering a "decade of accelerated growth," projected at $13.6 billion in 2026.

And GLP-1? Not a single presenter at CAGNY treated it as a threat. The unanimous framing was that it expands the addressable market — driving demand for high-protein, portion-controlled, fiber-rich products. 8% of US adults are on GLP-1 drugs today, heading to 10%+. That's not a headwind. That's a product design brief.

4. Frozen Is the New Fast Casual

If I asked you which aisle in the grocery store is the most innovative, you'd probably say snacks, or maybe beverages. But the answer from CAGNY 2026 is frozen.

The frozen case has quietly become the most exciting real estate in the store — where global cuisine, health innovation, and convenience converge. Smucker's Uncrustables brand is hitting $1 billion in annual net sales with a 20% ten-year CAGR. They've tripled monthly convenience store sales year-over-year. Conagra's frozen portfolio is 83% holding or gaining volume share.

And what's actually in the case now? P.F. Chang's Japanese BBQ chicken bowls. Empanadas (menu penetration up 8% YoY). No-seed-oil protein bowls. Indian cuisine (a $603M category growing at 10% three-year CAGR). Purple Carrot vegan meals. Steakhouse-quality sides. Mega breakfast bowls. Hand pies.

This isn't the sad Lean Cuisine aisle of a decade ago. It's a curated global food hall, priced for value, designed for convenience, and formulated for modern health. Frozen handhelds are up 7%. Frozen breakfast occasions have a 4% four-year CAGR. Frozen high-protein products represent a $13 billion category growing 13% in volume year-over-year.

If your brand isn't treating frozen as a primary innovation platform, you're leaving the most dynamic shelf space in the store to your competitors.

5. The Joy Dividend

This is the insight that ties the other six together.

Across every presentation at CAGNY — the winners and the ones struggling — a pattern emerged. Growth follows brands that deliver genuine emotional uplift: surprise, delight, comfort, belonging, identity. I'm calling it the Joy Dividend.

But joy doesn't maintain itself. It requires continuous investment. And the moment you stop feeding it — whether through complacency, cost-cutting, or never building it in the first place — decline begins.

The Joy Dividend Framework

Joy isn't a marketing veneer. It's a structural growth engine that compounds when invested in and decays when neglected.

Joy works when you keep investing in freshness, cultural relevance, and access.

Joy dies through complacency, cost-cutting, or never building it at all.

Joy shows up in three distinct forms across the CAGNY evidence:

Joy as Identity

Celsius — energy as belonging, lifestyle, and wellness ritual. 20% market share, +22% retail sales. 33% drink it socially. Cultural relevance across music, fashion, fitness, wellness.

Joy as Warmth

Dolly Parton × Conagra — consumers buy because Dolly makes them feel something. Not product superiority — cultural affection. Baking mixes up 16% YoY. Same playbook: Peanuts, BWW, Dr Pepper.

Joy as Experience

PepsiCo DRIPS craft beverage destinations and Doritos Loaded as a restaurant concept — social, shareable, immersive. The brand becomes a place, not just a product.

Where joy is driving growth:

Transformed energy from an emergency caffeine hit into a daily wellness ritual and social identity. Female consumers are especially routine-driven — morning joy, not afternoon desperation. Cultural relevance across music, fashion, fitness, and sports makes distribution a side effect of demand, not the cause of it.

Removed the last friction point — thaw time — so every Uncrustables moment is immediate. Tripled convenience store sales. Now in the top 10% of fastest-growing brands across all categories in the convenience channel. Joy here is barrier-free access to something beloved.

These products don't win on formulation. They win because Dolly Parton is one of the few figures in American culture who delivers uncomplicated warmth. The same pattern repeats across Conagra's mashup portfolio: Peanuts baking mixes, Buffalo Wild Wings × Slim Jim, Dr Pepper popcorn. Each is a cultural moment, not just a co-brand.

Where the joy dividend is being starved:

Hostess coasted on the product while the world demanded provocation. The brand still has recognition — Twinkies, Ding Dongs — but recognition without reinvention is a shrinking asset. Mark Smucker acknowledged "the path to stabilization is taking longer than we expected." Complacency is the quietest way to kill a joy brand.

Kraft Heinz optimized for margin and starved their brands of the energy that made them matter. Their $600M reinvestment and Canada turnaround prove recovery is possible — but re-injecting joy into a brand is slower and costlier than maintaining it. The lesson is clear: when you stop funding joy, you're not saving money. You're writing a much larger check that comes due later.

Newell never built emotional connection in the first place. Rubbermaid, Sharpie, Graco — functional brands with no joy strategy. The result is commodity positioning where the only lever is cost. Their turnaround is about building basic capabilities from near-zero. This is what happens when joy is never part of the equation.

6. Your Brand Is a Content Platform Now

The most successful CAGNY presenters aren't just launching products — they're launching cultural moments. And the line between their innovation pipeline and their content strategy has disappeared.

Celsius built a multi-brand platform that connects across music, fashion, fitness, sports, and wellness — earning 20% energy market share through cultural relevance, not just distribution expansion. Coca-Cola is personalizing FIFA World Cup campaigns at the city level — different creative for New York (European cultural affinities) versus Houston (Latin American) — powered by their modern marketing transformation. PepsiCo is turning Doritos into a restaurant concept, building DRIPS craft beverage destinations, and testing manufacturing through aggregator delivery in European cities. Conagra's celebrity mashup economy — Dolly, BWW, Dr Pepper, Wendy's, Peanuts — treats every collaboration as a cultural event designed for social virality.

The implication for brand leaders: your innovation pipeline and your content calendar need to operate as one system. If you can't tell the story of a new product in 11 seconds, you haven't finished developing it.

7. AI Isn't Your Marketing Department — It's Your Nervous System

Every company at CAGNY mentioned AI. But the most interesting applications weren't about generating marketing content. They were about sensing and responding faster than the competition.

Ingredion showed two sides of the same coin. Their texture business solves real-world problems like french fries going soggy in delivery — using ingredient science to maintain crispness and mouthfeel across new consumption occasions. And separately, they've built AI-powered predictive formulation that can predict consumer liking with 80-90% accuracy, cutting prototype development from 90 days to 15. Together, these capabilities form a solutions business that just crossed $1 billion in revenue. Conagra deployed real-time AI-enabled promotion optimization and saw +9 percentage points in promo lift in Q2 FY26 versus prior year. PepsiCo announced an NVIDIA and Siemens partnership for digital twin supply chain simulation — full factory modeling for bottleneck detection and capacity optimization. Coca-Cola is using digital for hyper-local consumer engagement at city-level granularity.

The pattern is clear: the winning use of AI in CPG isn't about making more content. It's about making better decisions, faster, at the point of action.

The Provocativeness Scorecard

Seven questions to ask your brand team on Monday morning:

- Are we earning attention — or just renting shelf space?

- Which consumer are we actually designing for — and have we abandoned the 'mainstream' fiction?

- Is health baked into our product architecture — or is it still a marketing claim?

- Are we treating frozen/convenience as innovation real estate — or as a legacy category?

- What is the joy our brand delivers — and have we refreshed it in the last 18 months?

- Does our innovation pipeline and content strategy operate as one system?

- Is AI making us faster at sensing and responding — or just generating more content?

Download the Full Presentation

Get the complete 18-slide deck with all the data, case studies, and the Joy Dividend framework — built in quiz format for your next team meeting.

Download the Deck →Source: Analysis of 21 CAGNY 2026 presentations and transcripts across 17 companies — Conagra, Coca-Cola, PepsiCo, Mondelez, Smucker, General Mills, Kraft Heinz, Celsius, Utz, Sysco, US Foods, Unilever, Reckitt, Newell, Kerry, IFF, and Ingredion. Data sourced from Circana, NielsenIQ, Euromonitor, Pew Research, and company filings. February 2026.